The thirty per cent line: how the mandatory bid rule protects and traps shareholders

Understand the mandatory bid rule, the 30 per cent control line and the moments it can both protect and trap UK shareholders during a takeover.

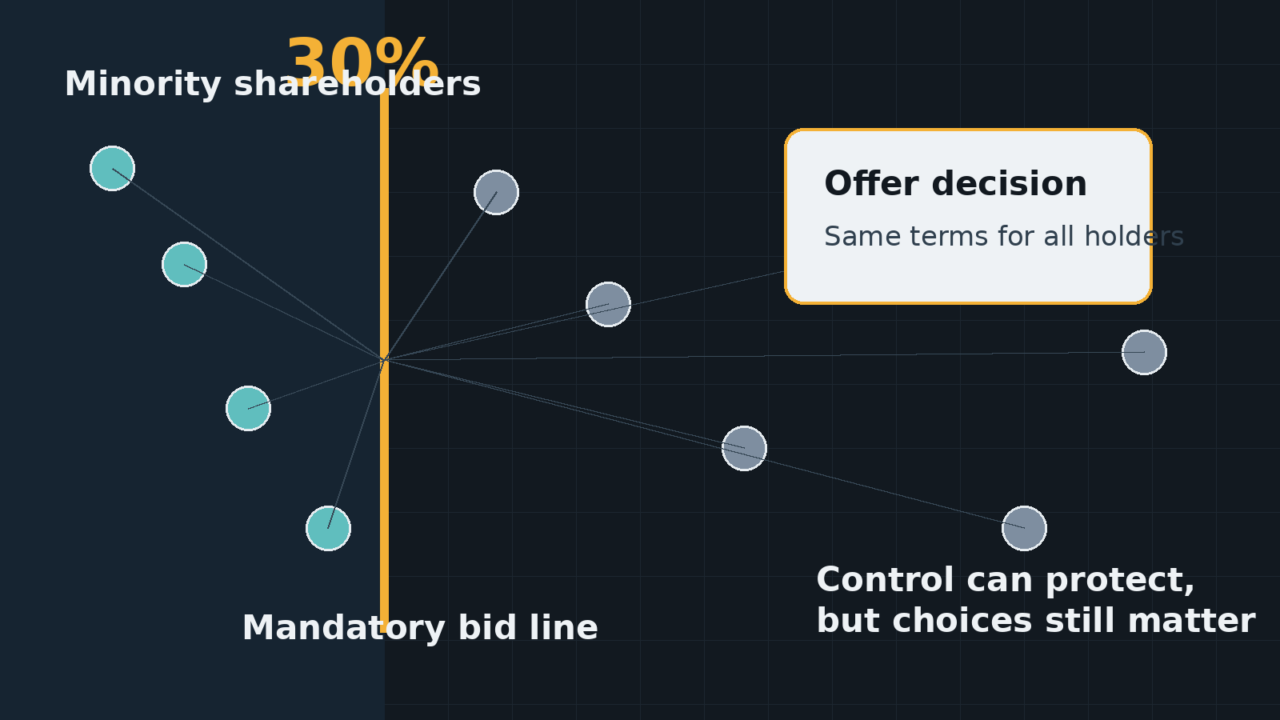

A single threshold determines when shareholders must be offered an exit route, but the same rule can leave minority investors stranded.

The Short Version

- The UK Takeover Code’s Rule 9 triggers a mandatory offer when a party reaches 30% of voting rights.

- This protection ensures fair treatment during control changes.

- Poorly structured bids can trap remaining shareholders in undervalued companies.

- Management ego often leads to value-destructive deals that bypass shareholder interests.

What the source says

The Street Smart Trader presents compelling evidence about the frequent failures of mergers and acquisitions to deliver shareholder value. Academic research referenced in the material indicates just 30% of deals create measurable benefits, with management vanity and flawed analysis frequently driving destructive transactions. The book’s historical bank-deal examples show a wider point: poor deal execution can damage shareholder value when executive confidence outruns sober analysis.

The source material reveals how deal terminology frequently obscures risks for ordinary investors. Phrases like “synergies” often conceal aggressive cost-cutting while ignoring operational challenges. As noted in the text, companies routinely misjudge the complexity of combining operations, with Stern School research showing only one quarter of mergers ever recoup their costs. This context helps explain why takeover regulations remain essential for protecting minority shareholders during corporate control changes.

Particularly relevant is the source’s focus on how deal momentum can overwhelm proper due diligence. One historical banking case in the source shows how even experienced management teams can succumb to pressure, with senior leadership later acknowledging that far more due diligence was needed. The lesson for this article is not the old number itself. It is that shareholders often learn the full risk only after the deal momentum has passed. Such examples demonstrate why regulatory frameworks must anticipate and mitigate these human factors in corporate decision-making.

Because the book was written before the current market setting, this article treats its examples as historical teaching material. The current rule discussion is anchored to the Takeover Panel and the Takeover Code, not to old market anecdotes as live evidence.

Why the thirty per cent line exists

The UK Takeover Panel established the 30% threshold in Rule 9 to mark the point where a shareholder gains effective company control. This clear benchmark prevents gradual acquisitions that could otherwise enable dominant shareholders to seize control without fair terms for minority investors. The rule acknowledges that beyond this level, remaining shareholders risk becoming trapped in companies where their interests may diverge from the controlling party.

The Panel’s approach stems from core principles of shareholder equality. When control changes hands, all investors should have equal opportunity to benefit from the premium typically paid for control. The 30% trigger enforces this by mandating any party crossing that line to offer all shareholders the highest price paid during the preceding twelve months.

Historically, this protection responded to corporate raiders in the 1960s and 1970s who quietly amassed controlling stakes before imposing their will on minority holders. The rule brings transparency and fairness to control changes, compelling acquirers to declare intentions upon reaching the threshold rather than accumulating shares covertly.

This mechanism creates a balanced playing field where all shareholders receive equal information and opportunity when control shifts. It prevents situations where insiders or institutional investors might exploit informational advantages at the expense of retail shareholders. The rule’s design ensures no shareholder group suffers disadvantage during these fundamental changes to company ownership and direction.

The threshold also represents a carefully considered balance between allowing normal market activity and preventing creeping control. Below 30%, investors can trade shares without triggering regulatory requirements. Above this level, the rules assume the shareholder’s intentions have shifted from investment to control, requiring corresponding protections for other investors.

How the rule protects shareholders

The mandatory bid rule serves three primary protective functions in the market. First, it stops stealth takeovers through gradual share accumulation below regulatory radar. Second, it guarantees minority shareholders equal treatment during control transitions. Third, it provides liquidity at fair valuation when new controlling shareholders emerge.

These protections gain particular relevance when considering the source material’s warnings about management overconfidence. Without Rule 9, dominant shareholders could push through major strategic changes while leaving minority investors with little practical influence at the moment control shifted. The mandatory offer provides an exit before such decisions impact company performance.

The rule also combats information imbalance in markets. Institutional investors and corporate insiders frequently possess better understanding of a company’s true worth than retail shareholders. The mandatory bid process ensures all shareholders receive identical information and equal exit opportunities during control changes.

Additional safeguards include the “chain principle” where acquiring control of a company that owns 30% of another may trigger further mandatory offers. This prevents rule circumvention through corporate structures. The Panel also monitors coordinated groups that might collectively cross the threshold through concerted action.

The protection extends to pricing mechanisms as well. By requiring the offer price to match the highest price paid during the previous twelve months, the rule prevents acquirers from offering different terms to different shareholder groups. This eliminates the potential for selective deal-making that could disadvantage certain investors.

Perhaps most importantly, the rule creates a clear decision point for shareholders. When control changes hands, all investors receive a formal offer they can evaluate independently. This contrasts with situations where control shifts gradually without such defined moments for shareholder decision-making.

How the trap can work

Ironically, the same regulation designed to protect shareholders can sometimes leave them exposed. When a mandatory offer fails to achieve 90% acceptance (required for compulsory acquisition), remaining investors may become locked into companies with altered strategic directions.

The source’s historical bank-deal discussion illustrates this risk clearly. Where hidden balance-sheet problems later emerge, earlier and clearer exit opportunities can look very different in hindsight. Instead, many holders can remain exposed inside a combined group whose risks are now harder to judge from the outside.

Another potential trap emerges when acquirers structure offers to technically avoid triggering the rule. Coordinated group arrangements or complex deal structures can sometimes achieve control without formally crossing 30%. While the Takeover Panel monitors these situations, determined acquirers occasionally exploit regulatory grey areas.

The situation becomes particularly problematic when management teams pursue acquisitions for personal prestige rather than shareholder benefit. As the source shows through older deal examples, executives can become intoxicated by deal-making, chasing transactions that make strategic sense only in their own minds. Shareholders who do not accept a mandatory offer can find themselves unwilling participants in expensive ventures they did not choose.

Post-offer scenarios often see reduced liquidity for remaining shares. With a controlling shareholder established, the free float decreases and institutional investors may reduce holdings, making it harder for remaining shareholders to exit at favourable prices later. This liquidity trap can persist for years after the initial offer period closes.

There’s also the risk of strategic divergence. The new controlling shareholder may pursue strategies that benefit their specific interests rather than all shareholders equally. This could include changes to dividend policy, asset sales, or operational restructuring that primarily serve the majority holder’s objectives.

There is another subtle trap. A mandatory offer can look clean because it gives everyone the same formal choice. In practice, each shareholder still faces a personal information problem. The offer document may describe the bidder’s intentions, but it cannot remove uncertainty about future dividend policy, debt levels, board influence, or the appetite of other investors to stay involved.

That is why the 30% line should be read as a decision point, not as a safety label. It tells shareholders that control may have changed. It does not tell them that accepting the offer is automatically wise, or that remaining invested is automatically foolish. The rule gives a framework for fair treatment, while the commercial judgement still belongs to the shareholder.

Worked example

Consider fictional UK retailer HomeStyle plc, trading at £2.00 per share. A private equity firm begins accumulating shares, reaching 29% without triggering disclosure requirements. They then purchase a single institutional block at £2.50 per share, crossing the 30% threshold.

Rule 9 now requires them to offer £2.50 to all shareholders. However, if only 60% accept, the remaining 40% become minority shareholders in a transformed company where:

- The controlling shareholder may prioritise debt repayment over growth initiatives.

- Dividend policies could undergo dramatic changes.

- Future corporate actions may primarily benefit the majority holder.

- Trading liquidity typically decreases substantially.

- Valuation multiples often contract due to reduced market interest.

This mirrors the source’s warning about how “control can move before small shareholders understand their practical choices.” Those who do not tender now own shares that may become harder to exit, potentially at lower valuations as market interest wanes.

The situation deteriorates further if the acquirer implements operational changes that serve their strategy but harm minority interests. They might dispose of profitable divisions to repay acquisition debt or shift business focus in ways that contradict original investment rationales. Minority shareholders have limited recourse beyond potentially complex legal action.

In our HomeStyle example, the private equity firm might add debt to extract quick returns, leaving remaining shareholders with a more indebted, riskier investment than they originally owned. The original £2.50 offer may start to look attractive compared to the company’s subsequent performance and reduced prospects.

What this means for you

Understanding Rule 9 helps investors evaluate takeover situations more critically. When mandatory offers emerge, consider these key evaluation points:

Acquirer’s historical conduct: Research how the bidding party has treated minority shareholders in previous transactions. Have they respected rights or pressured remaining holders?

Offer premium assessment: Does the offer price reflect the company’s long-term potential? Compare it to historical trading ranges and analyst projections.

Post-offer scenarios: What might the company resemble if you remain invested? Consider possible strategy shifts and their implications.

Management motivations: As the source material emphasizes, exercise particular caution when deals appear driven by executive vanity rather than clear business rationale.

The contrast in the source remains instructive without treating old cases as current facts. Some deals are planned with discipline, clear integration work and realistic assumptions. Others appear to be driven by prestige, speed and the fear of missing out. Shareholders bear the consequences when the second type wins.

Investors should also consider the broader market context. During periods of merger enthusiasm, as described in the source material’s analysis of earlier market cycles, deal quality can deteriorate as companies rush to participate in sector consolidation. Mandatory offers during such periods may represent the last clear exit before value destruction becomes apparent.

In plain English

The 30% rule functions like a warning bell for shareholders. When someone acquires that much of a company, everyone gets the chance to leave at a fair price. But just like real warning systems, sometimes people ignore the alert, leaving them stuck in problematic situations.

The rule tries to reduce situations where shareholders are locked into a damaging change of control before they have a clear, formal decision point. However, it’s not flawless. Sometimes investors find themselves owning stakes in fundamentally altered companies, with significantly reduced influence over operations.

Imagine a residential building where one purchaser acquires enough units to control the property. Regulations require them to offer all residents the same exit price. But those who remain may discover the new owner making changes they dislike, with limited ability to object. The kitchen you loved gets remodeled into something less functional, the garden you enjoyed gets paved over for parking, and your complaints carry little weight because you’re now in the minority.

This analogy captures the essential dilemma of the 30% rule. It provides protection at an important moment, but shareholders must still make active decisions about whether to stay or go. The rule creates the opportunity for fair treatment, but doesn’t eliminate the need for careful judgment about future prospects under new ownership.

Related reads

- Synergies: the polite word that can hide merger risk

- Mergers and acquisitions: who really wins

- The house broker: whose side is the company’s own broker on?

Investment education disclaimer: This article is for general education for UK readers. It is not financial, investment or tax advice.

This post is adapted from The Street Smart Trader. Used with permission.