The quality of earnings test for small-caps: how to tell if profits are real

Quality of earnings helps investors test whether small-cap profits turn into real cash. Learn the cash, working-capital and accounting checks that matter.

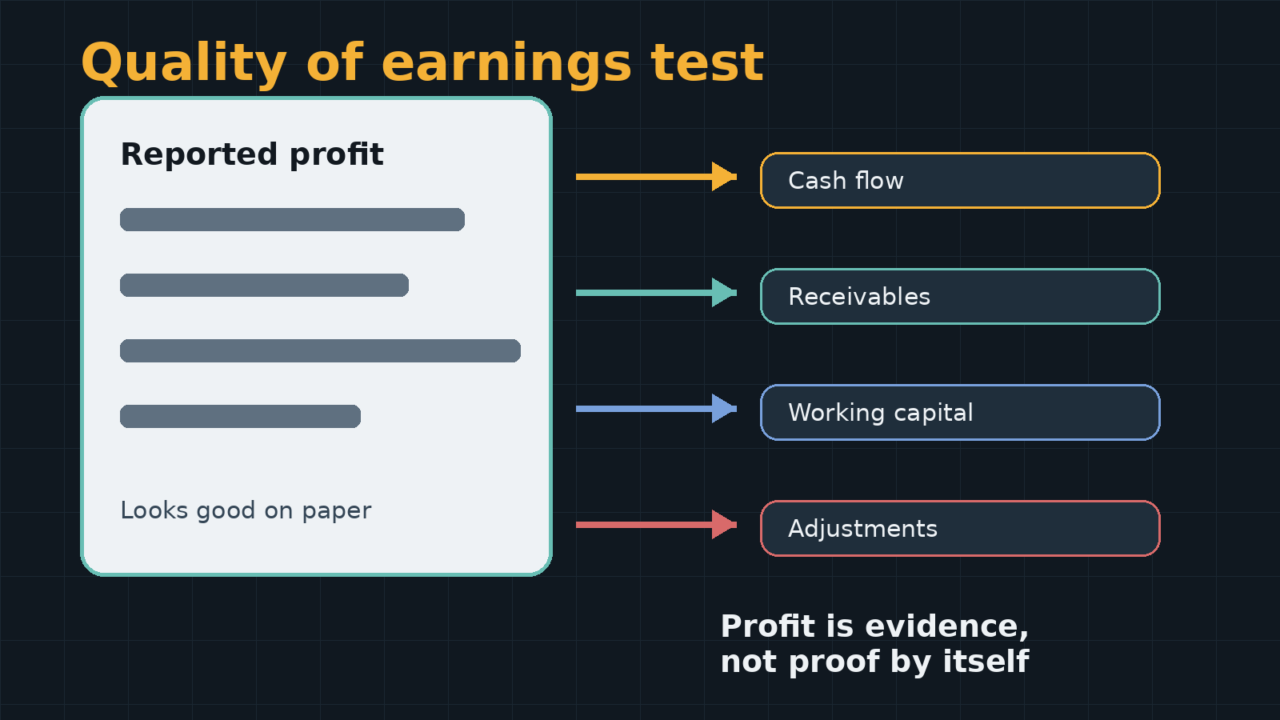

Small-cap profits can look impressive on paper while the underlying cash generation tells a very different story.

The Short Version

- Quality of earnings measures whether reported profits translate into actual cash that shareholders can rely on.

- Small caps often show rising profits while operating cash flow stagnates or falls due to working capital issues.

- Receivables growing faster than revenue, inventory buildups and capitalised costs can flatter earnings artificially.

- Testing cash conversion, working capital trends and accounting adjustments helps separate real profits from accounting optimism.

What the source is warning about

The Little Book of Small-Caps highlights how small companies can present compelling growth stories while fundamental weaknesses lurk beneath the surface. Unlike large-cap companies with established cash flows and institutional oversight, small caps operate with less scrutiny and often face pressure to show progress to maintain investor confidence and access to funding.

This pressure can lead to accounting choices that maximise reported profits in the short term while obscuring underlying cash generation problems. The book emphasises that warning signs often appear in financial statement details rather than headline numbers, requiring investors to dig deeper than surface-level profit figures.

Small caps have less room for error than established companies. A working capital crisis or cash flow shortfall that might be manageable for a FTSE 100 company could prove fatal for a small cap with limited banking facilities and no established credit lines. This makes the quality of reported earnings particularly crucial when evaluating smaller companies.

What quality of earnings means

Quality of earnings refers to how much of a company’s reported profit represents genuine economic value creation that translates into cash the business can actually use. High-quality earnings convert reliably into operating cash flow, while low-quality earnings may exist primarily on paper through accounting treatments that defer cash collection or accelerate revenue recognition.

For small caps, this distinction matters enormously because these companies often depend on external funding to grow. If reported profits don’t generate corresponding cash, the business may need to raise capital more frequently or at worse terms than investors expect. This can lead to dilution, higher borrowing costs, or in extreme cases, financial distress.

Quality of earnings analysis examines the gap between what the income statement reports and what the cash flow statement reveals. A widening gap suggests that profits may be less reliable than they appear, potentially indicating aggressive accounting, deteriorating business fundamentals, or both.

The concept becomes particularly important in small caps because these companies typically have fewer resources to weather periods where profits don’t convert to cash. Large companies might manage working capital fluctuations through established banking relationships, but small caps often lack such flexibility.

The cash conversion test

The most direct way to test earnings quality is comparing reported operating profit to operating cash flow over time. High-quality earnings should show operating cash flow that tracks closely with operating profit, allowing for normal fluctuations in working capital and timing differences.

Operating cash flow represents the actual cash generated by the business after paying suppliers, employees, and other operating expenses. Unlike reported profit, it cannot be manipulated through revenue recognition timing or non-cash accounting adjustments. If operating cash flow consistently lags behind reported profits, this suggests the earnings may not be as solid as they appear.

For small caps, sustained negative operating cash flow while reporting profits often indicates serious underlying issues. The company may be growing receivables faster than it can collect them, building inventory that isn’t selling as quickly as expected, or using accounting treatments that recognise revenue before cash actually arrives.

Investors should examine cash conversion ratios over multiple periods rather than single quarters, as small caps can experience significant seasonal variations or lumpy customer payment patterns. However, a persistent trend of poor cash conversion typically signals fundamental problems with the business model or execution.

Working capital: where profits can hide

Working capital movements often explain the gap between reported profits and cash generation in small caps. When receivables grow faster than revenue, it suggests the company may be extending credit terms to boost sales, collecting payments more slowly, or potentially recognising revenue prematurely.

Inventory buildups present another red flag, particularly for small caps without sophisticated supply chain management. Rising inventory levels relative to sales may indicate slowing demand, obsolete stock, or poor inventory management. While some inventory growth is normal for expanding businesses, disproportionate increases often signal problems.

Payables can also distort the picture. Small caps sometimes manage cash flow by extending payment terms with suppliers, which can temporarily boost operating cash flow while creating future obligations. This strategy has limits, as suppliers may eventually demand faster payment or refuse to extend further credit.

The working capital cycle becomes particularly important for small caps because they typically have less negotiating power with both customers and suppliers compared to larger companies. A small cap that extends generous payment terms to win business may find itself funding customer operations while struggling to collect cash for its own needs.

Seasonal businesses require special attention to working capital patterns. A retailer might legitimately build inventory before peak selling seasons, but the subsequent cash conversion should demonstrate that the inventory investment was justified by actual sales rather than optimistic projections.

Capitalised costs and adjusted profit

Small caps often capitalise development costs, marketing expenses, or other expenditures that might be expensed immediately by larger companies. While this treatment may be technically correct under accounting standards, it can flatter reported profits by deferring the impact of cash outflows.

Software companies frequently capitalise development costs, spreading the expense over several years rather than recognising it immediately. This creates a timing difference where current profits appear higher while future periods will bear the amortisation expense. If the capitalised development doesn’t generate expected returns, the company may face impairment charges that reverse previous profit recognition.

Adjusted profit measures have become increasingly common among small caps, with companies presenting EBITDA or adjusted earnings figures that exclude various costs deemed non-recurring or non-cash. While some adjustments may be legitimate, excessive use of adjusted metrics can obscure the true cost of running the business.

Acquisition-related costs, restructuring charges, and share-based compensation are frequently excluded from adjusted profit calculations. However, for small caps that regularly make acquisitions or frequently restructure operations, these “exceptional” costs may actually represent normal business expenses that should be considered when evaluating profitability.

The key question for investors is whether adjusted metrics provide genuine insight into underlying business performance or simply present a more flattering picture of financial results. Companies that consistently report adjusted profits significantly higher than statutory profits may be using these measures to distract from fundamental performance issues.

Worked example: profit up, cash down

Consider a fictional small-cap technology company, TechGrow Ltd, which reports the following results over three years:

Year 1: Revenue £5 million, operating profit £500,000, operating cash flow £400,000, trade receivables £800,000

Year 2: Revenue £7 million, operating profit £800,000, operating cash flow £300,000, trade receivables £1.4 million

Year 3: Revenue £9 million, operating profit £1.1 million, operating cash flow £200,000, trade receivables £2.1 million

At first glance, TechGrow appears to be performing well, with revenue growing 80% over three years and operating profit more than doubling. However, the cash flow picture tells a different story. Operating cash flow has actually declined by 50% despite the profit growth, suggesting serious quality of earnings issues.

The receivables data reveals the problem. Trade receivables have grown from 16% of annual revenue in Year 1 to 23% in Year 3, indicating that customers are taking longer to pay or the company is extending more generous credit terms to drive sales growth. The additional £1.3 million tied up in receivables over the three-year period largely explains why cash flow has deteriorated while profits increased.

This pattern suggests TechGrow may be recognising revenue before collecting cash, potentially through extended payment terms or aggressive revenue recognition policies. While the company reports growing profits, it’s actually generating less cash each year, which could create funding pressures if the trend continues.

For a small cap like TechGrow, this deteriorating cash conversion could prove problematic if the company needs additional funding for growth or faces unexpected expenses. The apparent profit growth may not represent genuine value creation if customers ultimately cannot or will not pay their outstanding balances.

A practical checklist for readers

When evaluating small-cap earnings quality, investors can examine several key indicators without requiring advanced accounting knowledge. These checks help identify potential red flags before they become serious problems.

Compare operating cash flow to operating profit over multiple periods. Consistently negative operating cash flow while reporting profits warrants investigation. Look for explanations in management commentary and cash flow statement details.

Calculate receivables as a percentage of revenue and track this ratio over time. Rising receivables relative to sales may indicate collection problems or aggressive revenue recognition. Similarly, monitor inventory levels relative to cost of sales to identify potential obsolescence or demand issues.

Examine the cash flow statement’s working capital section to understand what’s driving cash flow changes. Large increases in receivables or inventory without corresponding business growth often signal problems.

Review capitalised costs and development expenditure on the balance sheet. Significant increases in these items may indicate that current profits benefit from deferred expense recognition. Consider whether the capitalised amounts are likely to generate future returns.

Compare statutory profit to adjusted profit measures. Large or growing differences may suggest that “exceptional” costs are becoming routine business expenses that management prefers to exclude from headline figures.

Monitor debt levels and available cash relative to operating cash flow. Small caps with poor cash conversion may face funding pressures that could lead to dilutive equity raises or restrictive debt arrangements.

Read management commentary carefully for explanations of working capital movements and cash flow trends. Vague explanations or frequent changes in accounting policies may indicate attempts to obscure underlying performance issues.

Related Reads

Earnings quality sits alongside other small-cap checks such as cash runway, promotional language and operational evidence. Compare it with our guide to pre-revenue small caps and our explainer on how to read mining exploration results when the story depends heavily on future potential.

- Pre-revenue small caps: why normal valuation rules often fail

- How to read mining exploration results

- What happens when institutions start buying a small-cap?

In plain English

Quality of earnings analysis helps investors distinguish between companies that generate genuine cash profits and those that primarily create accounting profits. For small caps, this distinction can mean the difference between sustainable growth and eventual financial distress.

The fundamental principle is simple: profits should eventually convert to cash that the business can use to fund operations, invest in growth, or return to shareholders. When this conversion consistently fails to occur, it suggests that reported profits may not represent real economic value creation.

Small caps face particular challenges in this area because they often lack the financial resources and institutional oversight that help larger companies manage working capital efficiently. A small cap that extends generous payment terms to win business may find itself inadvertently financing customer operations while struggling to fund its own growth.

Investors should remember that small-cap investing involves significant risks, including the possibility of total loss. Companies with poor earnings quality face additional risks related to potential funding difficulties, accounting restatements, or business model sustainability. Quality of earnings analysis provides one tool for identifying these risks, but it cannot eliminate the inherent uncertainties of small-cap investing.

The goal is not to find perfect companies, which rarely exist in the small-cap universe, but to understand the quality and sustainability of reported financial performance. This understanding helps investors make more informed decisions about the risks and potential rewards of small-cap investments.

Investment education disclaimer: This article is for general education for UK readers. It is not financial, investment or tax advice.

This post is adapted from The Little Book of Small-Caps. Used with permission.