Active vs Passive Investing: The Honest Version

Active vs passive investing is really a choice about cost, judgement and portfolio role. Learn how UK beginners can compare the trade off honestly.

Active vs passive investing sounds like a simple contest. One side tries to choose the better investments. The other follows a market index and accepts the result. In reality, the useful question is not which side wins every time. It is what each approach is trying to do, what it costs, what can go wrong, and how a beginner can think about the trade off without turning it into a team sport.

The argument never ends because both sides have evidence they can point to. Some active managers have protected capital, found overlooked opportunities, or navigated unusual markets well. Many passive funds have delivered broad exposure at low cost and have avoided the risk of paying more for a manager who fails to add value. The honest version is that neither label removes risk, and neither label makes the investor’s job disappear.

The short version

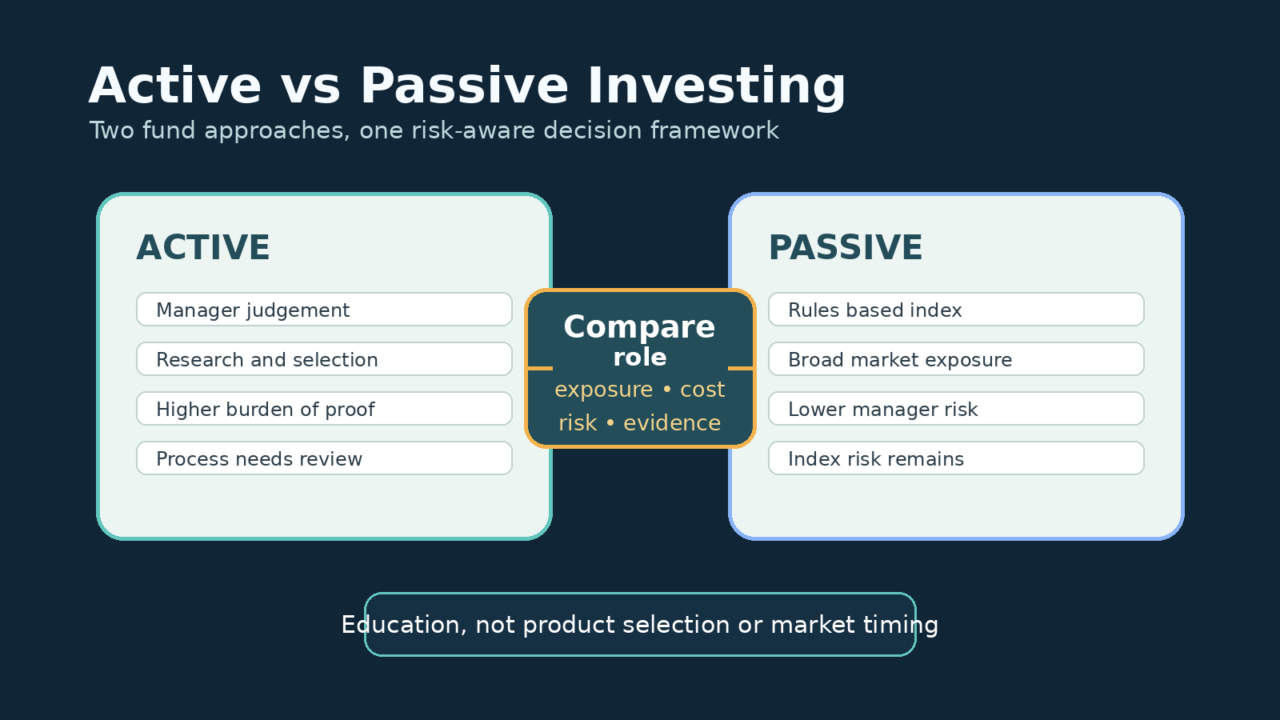

Passive investing usually means using a fund that tracks an index, such as a broad share market or bond market benchmark. The fund is not trying to decide which companies are best. It is trying to follow a set of rules. Active investing usually means paying a manager to make judgement calls about what to include, avoid, overweight, underweight, or trade as conditions change.

For a beginner, the biggest difference is not glamour. It is burden of proof. A passive fund asks whether the index is a sensible exposure for the role it plays in a portfolio. An active fund asks that question plus several more: whether the manager has a repeatable edge, whether costs are justified, whether the process still works, and whether the investor can stay patient when performance looks disappointing.

What passive really means

Passive does not mean risk free, automatic, or sensible in every context. It means rule-following. A global equity tracker, for example, may give wide exposure across countries and sectors, but it still rises and falls with equity markets. A bond tracker can fall when interest rate expectations move. A narrow sector tracker can be passive and still highly concentrated.

The appeal is clarity. The investor can usually see the benchmark, understand the broad exposure, compare costs, and know that the fund is not trying to make a series of private judgement calls. That can be helpful for beginners because fewer moving parts make it easier to see what is driving results.

The weakness is that an index does not ask whether a price is sensible. It includes securities because they fit the index rules. If a company or sector becomes a larger part of the index, a tracker reflects that weight. If a market has a long weak period, the passive investor experiences it. Passive investing removes manager-selection risk, but it does not remove market risk.

What active really means

Active investing means a manager is making choices. Those choices might involve company research, valuation work, macro views, risk controls, income targets, credit analysis, or a specific style such as value, quality, growth, smaller companies, or defensive assets. The manager may look very different from the index, or only slightly different.

The appeal is judgement. A strong active manager may avoid some weak areas, identify opportunities before they become widely accepted, manage concentration, or change positioning as evidence changes. Active can also make sense in areas where the market is less researched, less liquid, or harder to capture neatly through a broad index.

The weakness is that judgement can be wrong. Costs are usually higher. Performance can lag for long periods. A fund can drift away from the process that made it attractive. A star manager can leave. A strategy can become too large for the opportunity it is trying to capture. Active investing does not just ask whether a market is worth exposure. It asks whether a particular decision-making process is worth paying for.

Why the argument gets noisy

The debate often becomes noisy because people compare the wrong things. A cheap global tracker is not the same job as an active smaller companies fund. A cautious multi-asset fund is not the same job as a high-conviction equity fund. A manager who underperforms for one year has not automatically failed, and a tracker that has done well during a strong market has not proven it is safe.

Time period also matters. Many performance charts start and end at convenient points. A fund can look excellent over five years and ordinary over ten. It can look poor after a style goes out of favour and then recover when the market environment changes. Beginners should be careful with any chart that quietly chooses the most flattering window.

Costs matter because they are one of the few variables investors can see before the result arrives. A higher charge does not make a fund bad by itself, but it raises the hurdle. The manager has to overcome that extra drag before the investor sees any benefit. Related costs, including platform and dealing costs, can matter too, which is why platform fees can change the net result.

A practical way to compare them

A useful comparison starts with the job the fund is meant to do. Is it the core of a long-term portfolio, a diversifier, an income component, a cautious allocation, or a specialist satellite? The answer changes the standard you apply. A broad core fund needs to be understandable, durable, appropriately diversified, and cost aware. A specialist active fund needs a clearer reason for existing because it adds more manager judgement.

Next, compare exposure before comparing recent returns. Two funds can have similar names but very different holdings, regions, sectors, currencies, or risk levels. If one fund owns the whole market and another owns a concentrated list of companies, their performance gap may simply reflect different exposures. That is not automatically skill or failure.

Then look at process. For passive funds, ask how the index is built, whether the fund tracks it closely, what it costs, and whether the benchmark fits the role. For active funds, ask what the manager is trying to exploit, how disciplined the process is, how much freedom the manager has, and what would count as evidence that the original case has weakened.

Finally, think about behaviour. Some investors choose a low-cost passive core because it reduces the temptation to chase every new idea. Others use a limited active allocation where they believe the manager’s approach is understandable and worth monitoring. Both choices can be reasonable if they are consistent with the investor’s plan, time horizon, and risk tolerance.

Common beginner mistakes

The first mistake is assuming passive means basic and active means sophisticated. A complicated passive product can still be hard to understand. A plain active fund can still follow a clear process. The label is a starting point, not a quality stamp.

The second mistake is treating past performance as the whole argument. Returns matter, but they need context. Was the fund taking more risk? Did it benefit from one sector, one region, one style, or one unusually strong position? Did the investor experience the full period shown in the chart, or only the difficult part after joining late?

The third mistake is collecting too many funds that all do the same thing. Owning five funds does not guarantee diversification if they share similar holdings or drivers. That is why diversification can still fail if the underlying investments overlap.

The fourth mistake is ignoring time horizon. A fund that is reasonable for long-term money can be unsuitable for cash needed soon. Market falls do not wait for a convenient moment. Before comparing active and passive funds, beginners should separate short-term cash needs from long-term investing money. Cristoniq has a separate guide on why money needed soon should be treated differently from long-term investing money.

When active may have a clearer case

Active may deserve closer attention where the fund’s role depends on judgement that an index cannot provide. That might include controlling downside risk, navigating less liquid markets, applying a specific valuation discipline, selecting credit risk carefully, or focusing on a specialist area that broad trackers do not capture neatly.

Even then, the case should be specific. Saying a manager is experienced is not enough. A beginner can ask: what does this manager do differently, why might it work, what could make it fail, how expensive is it, and how would I judge the result without reacting to every short-term setback?

Active also requires monitoring. Not daily checking, but periodic review. Has the manager changed? Has the fund become much larger? Has the process drifted? Are costs still reasonable? Does the fund still fit the job it was chosen for? If the only reason is that it recently performed well, the case is probably too thin.

When passive may have a clearer case

Passive may have a clearer case where the investor wants broad exposure, low cost, transparent rules, and fewer manager-specific decisions. It can be especially useful as a core building block because it makes the portfolio easier to understand. The investor can spend more time on asset mix, risk level, time horizon, and behaviour rather than trying to identify the next winning manager.

The trade off is acceptance. A passive investor accepts the index’s composition and the market’s ups and downs. If a sector becomes expensive, the tracker does not step aside. If the index is concentrated in a few large companies, the tracker reflects that. If the market falls, the fund participates. Passive investing is simple in structure, but not emotionally easy.

A balanced decision framework

One practical framework is to ask four questions.

- Role: What job should this fund do in the wider portfolio?

- Exposure: What market, asset class, region, sector, or style does it actually represent?

- Cost: What drag is visible before any future return arrives?

- Evidence: What would make the original case stronger or weaker over time?

If those questions are hard to answer, the fund may be harder to own calmly. The FCA’s InvestSmart material encourages investors to pause and ask basic questions before committing money, including whether they understand the investment and the risk involved. That mindset is useful here. The active versus passive label should never replace the more basic question: do I understand what I am exposed to and why it belongs in the plan?

In plain English

Active investing is paying for judgement. Passive investing is paying for rules-based exposure. Active can add value, but the investor needs a clear reason to believe the process is worth the extra cost and monitoring. Passive can be efficient, but the investor still takes the market risk that comes with the index.

The honest answer is not that one side is always right. The honest answer is that a beginner should understand the job, exposure, cost, risk, and evidence before choosing any fund. A simple passive core can be sensible for some plans. A carefully chosen active fund can be useful for some roles. A messy collection of funds chosen from recent performance can be weak whether the labels say active, passive, or both.

Investment education disclaimer: This article is for general education only. It is not personal financial advice and does not tell you what action to take with any specific investment, fund, account, broker or platform. Investments can fall as well as rise, and you may get back less than you put in. Tax treatment and account rules depend on individual circumstances and can change. If you are unsure, consider regulated financial advice.

Related Reads

- Pound cost averaging explained

- Diversification investing: why spreading risk matters

- Making sure your broker is FCA authorised

This article is for general information and financial education only. It is not personal investment advice, tax advice, legal advice or a recommendation to buy or sell any investment. The value of investments can go down as well as up, and you may get back less than you invest. Tax rules can change and their effect depends on your circumstances. If you are unsure, seek guidance from a qualified financial adviser.