Crypto Travel Rule: What Data Gets Shared in Transfers

The crypto Travel Rule can add names, checks and delays to transfers. Learn what firms share, when friction appears and what users should check first.

The crypto Travel Rule is one of the least glamorous parts of crypto, but it is one of the rules ordinary users are most likely to notice. It explains why a transfer that feels like a simple wallet movement can suddenly ask for extra names, addresses or account details.

The Short Version

- The crypto Travel Rule makes regulated firms collect and share more sender and beneficiary information around some transfers.

- The blockchain transaction and the compliance review are separate layers, which is why a transfer can confirm on-chain but still be delayed by a platform.

- Most user friction appears when exchanges, custodians or other firms are involved, not when two self-custody wallets simply broadcast a transaction.

- Names, provider details and wallet checks matter because missing or mismatched information can slow, reject or hold the transfer.

What the Travel Rule changes

The Travel Rule is a data sharing requirement for firms that move crypto on behalf of customers. In plain English, certain crypto businesses are expected to collect and pass on information about the person sending crypto and the person receiving it. The rule is not about predicting prices, ranking tokens or deciding whether crypto is good or bad. It is about making transfers easier to trace when regulated firms are involved.

The important word is firm. A regulated exchange, broker, custodian or payment-style crypto business can be treated as a virtual asset service provider, often shortened to VASP. A personal wallet that a user controls directly is different from a business that holds accounts, runs compliance checks and processes transfers for customers. In practice, most user friction appears when a transfer touches an exchange or custodian rather than when two self-custody wallets simply broadcast a blockchain transaction.

The policy idea is borrowed from banking. When money moves through the banking system, the institutions handling the payment do not only pass value. They also pass certain information about the payer and payee. Crypto transfers created a harder version of that problem because public blockchains show addresses and transaction hashes, not the real-world customer data that compliance teams may need.

For a UK reader, the practical point is not that every blockchain transaction suddenly exposes all personal details publicly. It does not. The point is that the regulated business handling the transfer may need to ask for information, check it, store it and sometimes transmit it to another regulated business. That can change what the user sees at the point of withdrawal, deposit or transfer review.

The moving parts in a Travel Rule transfer

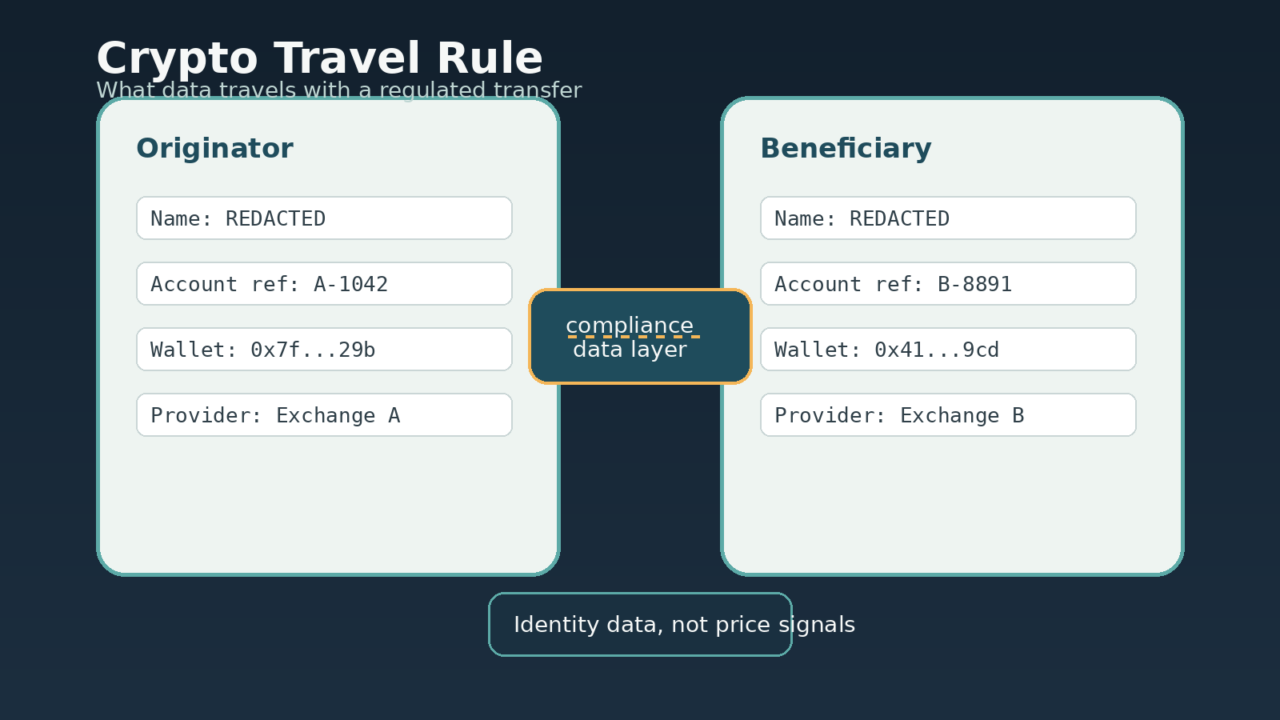

There are four moving parts: the sender, the receiver, the sending firm and the receiving firm. Regulatory language often calls the sender the originator and the receiver the beneficiary. If both sides use regulated firms, those firms may need enough information to understand who is behind the transfer and where the crypto is going. If one side uses a self-hosted wallet, the firm may still need to ask extra questions about wallet ownership or purpose.

The exact information can vary by jurisdiction, transfer type, provider policy and risk assessment. A simple version might include the sender’s name, account reference, wallet address and sometimes address or customer identification details. It can also include beneficiary information such as name, account reference, wallet address or other identifying information. The point is not that every field appears in every transfer. The point is that the transfer is no longer judged only by the blockchain address.

There is also a timing issue. Blockchain networks can settle quickly, but compliance checks do not always feel instant. A sending firm may need to gather information before release. A receiving firm may need to match incoming data with a customer account before crediting the deposit. If the information is missing, mismatched or inconsistent, the transfer can be delayed, rejected or held for review.

Think of the transfer as two layers. The blockchain layer moves tokens between addresses. The regulated firm layer decides whether customer information is complete enough to allow the business to process, credit or release the transfer. Confusion happens when a user sees the blockchain transaction and assumes that the business side must be finished too. Those are related, but not identical.

A simple example

Imagine Maya wants to send crypto from exchange A to exchange B. She enters the receiving address from exchange B and starts the withdrawal. In a no-friction version of crypto, that might be enough. Under a Travel Rule process, exchange A may ask whether the receiving address belongs to Maya, to another person or to another provider. It may ask for the beneficiary name, the receiving provider or a reason for the transfer. Exchange B may also check the incoming transfer before crediting Maya’s account.

If Maya enters her own name consistently, uses the right receiving address and the receiving provider recognises the transfer information, the process may be barely noticeable. If the names do not match, the receiving provider cannot identify the account, or Maya says the wallet belongs to a third party but gives incomplete details, the transfer may slow down. The blockchain has not necessarily failed. The compliance package around the transfer is incomplete.

Now imagine Maya is withdrawing to a self-custody wallet. There may be no receiving provider to exchange information with. The sending firm may still ask whether Maya controls the wallet and may use its own risk checks. That can feel odd to someone who thinks wallet addresses are enough. The firm is trying to connect a real customer relationship to an address that, on chain, is only a string of characters.

This is why Travel Rule friction can seem inconsistent. One transfer is smooth. Another transfer of similar size triggers questions. A third transfer is held because the receiving provider uses a different data format or because the customer details do not match cleanly. That inconsistency does not prove that a provider is safe or unsafe. It shows that compliance systems, risk policies and data standards still vary.

Where transfers slow down

The data generally sits in three groups. First is identity data: names, customer references and sometimes address or identification information. Second is transfer data: wallet addresses, transaction references, amount, asset type and provider details. Third is relationship data: whether the sender and receiver are the same person, whether the transfer is to a business, whether a third party is involved and whether the destination is a self-hosted wallet.

That does not mean the information is written onto the public blockchain. A blockchain explorer may show addresses, transaction hashes, block numbers and amounts, but the extra customer information is normally handled by firms through their own systems or compliance messaging tools. Cristoniq’s guide to blockchain explorers is useful here: explorers can show the on-chain trail, but they do not reveal everything a regulated platform knows about its customer.

Privacy concerns are still real. More data collection means more records that must be protected, corrected and governed. If a provider collects more information than necessary, stores it poorly or shares it with weak controls, the user carries a new data risk. If it collects too little, transfers can become harder to process and suspicious activity can be harder to investigate. The policy trade off is between traceability, privacy, financial crime controls and usable transfers.

Users should also understand the difference between pseudonymity and anonymity. A public address is not automatically a real-world name, but it can be linked to patterns, exchanges, deposits, withdrawals and other information. Cristoniq’s guide to privacy coins explains why regulators pay close attention to systems that make tracing harder. The Travel Rule sits in the same broad tension between privacy and accountability, although it works through regulated businesses rather than directly changing a blockchain.

What This Means For You

Delays usually come from missing, mismatched or high-risk information. A name may be spelled differently across two accounts. A provider may not recognise the receiving firm. A wallet may be linked to activity that triggers extra review. A customer may be sending to a destination that the firm does not support. A transfer may fall outside the provider’s normal risk appetite. None of those points automatically means a user has done anything wrong.

There are also operational reasons. The sending provider and receiving provider may use different vendors or workflows for Travel Rule messaging. The receiving provider may need manual review before crediting a deposit. A system may ask for more information after a user thought the withdrawal was finished. A provider may reject a transfer rather than accept incomplete data. This is frustrating, but it is not the same as a blockchain reversal. It is a business processing decision around a transfer.

Users can reduce avoidable friction without treating this as financial advice. The practical checks are administrative: confirm the receiving address, use the name that matches the receiving account, keep records of the transfer reference, read the provider’s instructions before sending, and avoid guessing if the form asks who controls the wallet. If the transfer is for someone else, the form may need different information from a self-transfer.

It is also sensible to test operational processes with small, low-stakes transfers where appropriate, but that is a process check, not a recommendation to use any specific token, exchange, wallet or platform. The more important habit is to understand what the provider is asking for before moving value. If a provider cannot clearly explain why information is needed, what happens to it and how errors are corrected, that is a service-quality warning sign.

In Plain English

The Travel Rule does not publish your full identity on the blockchain. It changes what regulated firms may need to ask, store and share before they are comfortable processing a transfer. If a platform asks extra questions, it is usually dealing with compliance checks around the movement, not changing how the chain itself works.

Related Reads

Do not assume that an on-chain confirmation means the receiving account will credit instantly. The blockchain may show settlement while the provider still reviews the customer data. Do not assume that a wallet address proves ownership. A provider may still ask who controls the address. Do not assume that all providers apply the same thresholds or data fields. Rules, local implementation and business policy can differ.

Do not assume that more compliance language means a platform is safer. A clean interface can still have weak support, poor data handling or slow dispute resolution. Equally, a provider that asks extra questions is not automatically suspicious. It may be following a regulatory process or its own risk controls. The useful question is whether the request is understandable, proportionate and backed by clear support.

Do not assume that Travel Rule checks remove crypto risk. They do not protect a user from sending to the wrong address, misunderstanding network fees, choosing the wrong network, falling for social engineering or holding an asset that falls in value. For transaction mechanics, Cristoniq’s guide to crypto transaction hashes explains why a transaction reference is useful evidence but not a guarantee that every off-chain account process is complete.

The Travel Rule is best understood as a compliance layer around certain transfers, not as a safety seal. It can improve traceability for regulated firms, but it cannot make a bad destination good, a risky asset safe or an unsupported transfer recoverable. That distinction matters because users often mix up compliance approval, technical completion and economic safety.

What this means in practice.

Before using a provider for transfers that may trigger extra checks, read the transfer rules in plain language. Look for the supported networks, whether self-hosted wallets need ownership confirmation, what beneficiary information is requested, what happens if details are wrong, how long reviews usually take and how support handles rejected transfers. Those are practical service questions, not trading signals.

If a form asks for information that seems excessive, pause and read the provider’s explanation. The right response is not to invent details. Incorrect beneficiary information can create a bigger problem than a delayed transfer. If the provider’s wording is unclear, use its support route and keep copies of the transfer reference, wallet address and instructions. Records matter when a transfer is delayed.

For teams or businesses, the checklist is more formal. Keep customer instructions separate from internal notes, record who supplied beneficiary details, avoid sharing more personal data than the transfer requires, and decide who can approve exceptions. If a business is moving crypto for customers, it needs specialist compliance advice. A general explainer is not enough for designing regulated processes.

The bottom line is simple. The Travel Rule adds a real-world identity and compliance layer to some crypto transfers. It can mean more questions, slower processing and more data handling. It does not mean every detail becomes public, and it does not remove the ordinary risks of using crypto. Treat it as a reason to prepare cleaner transfer information, keep better records and avoid rushing through forms that affect where value goes.

Crypto risk reminder: Cryptoassets are high risk and can be volatile. This article is for general education for UK readers. It is not financial advice, investment advice, tax advice or legal advice. It does not recommend buying, selling, holding or using any token, exchange, wallet or platform.

Disclaimer: Cryptocurrency investments are highly volatile and speculative. Their value can rise and fall sharply, and you could lose all of your investment. This article is for informational and educational purposes only and does not constitute financial advice. Always do your own research before making any investment decision.